As healthcare costs continue to rise, Health Savings Accounts (HSAs) remain one of the most valuable tools for setting aside tax-advantaged dollars for future medical expenses.

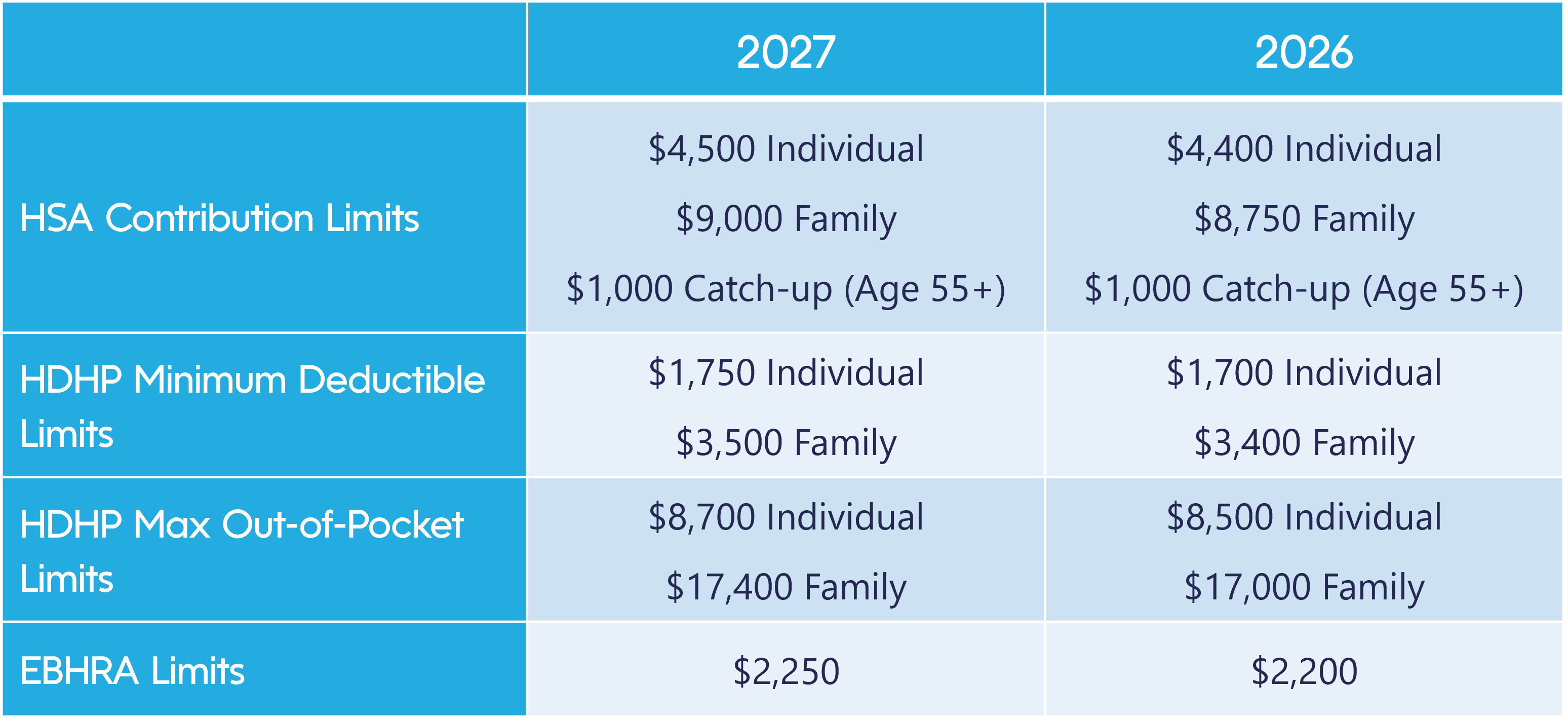

On May 29, 2026, the IRS announced the annual inflation-adjusted limits for HSAs, High-Deductible Health Plans (HDHPs), and Excepted Benefit Health Reimbursement Arrangements (EBHRAs), with most limits increasing for 2027. These annual adjustments give employees additional opportunities to save for healthcare expenses while helping employers prepare for 2027 benefit and payroll planning.

HSA Catch-Up Contributions

Individuals who are age 55 or older by the end of the tax year may contribute an additional $1,000 to their HSA beyond the standard annual contribution limit. The catch-up amount remains unchanged for 2027.

For example, an individual age 55 or older with self-only HDHP coverage may contribute up to $5,500 in 2027 ($4,500 standard contribution limit plus the $1,000 catch-up contribution).

Looking Ahead

Employers sponsoring HDHPs and employees who contribute to HSAs should review these new limits as they prepare for 2027 enrollment and payroll contribution elections. The increased limits may provide additional opportunities for tax-advantaged healthcare savings in the coming year.